The tech company sees currency headwinds persisting but not enough to topple its booming cloud business. Is it a buy?

Shares of cloud computing company Oracle (ORCL) are climbing Tuesday after the company topped earnings and revenue estimates for the quarter and signalled strong revenue growth ahead.

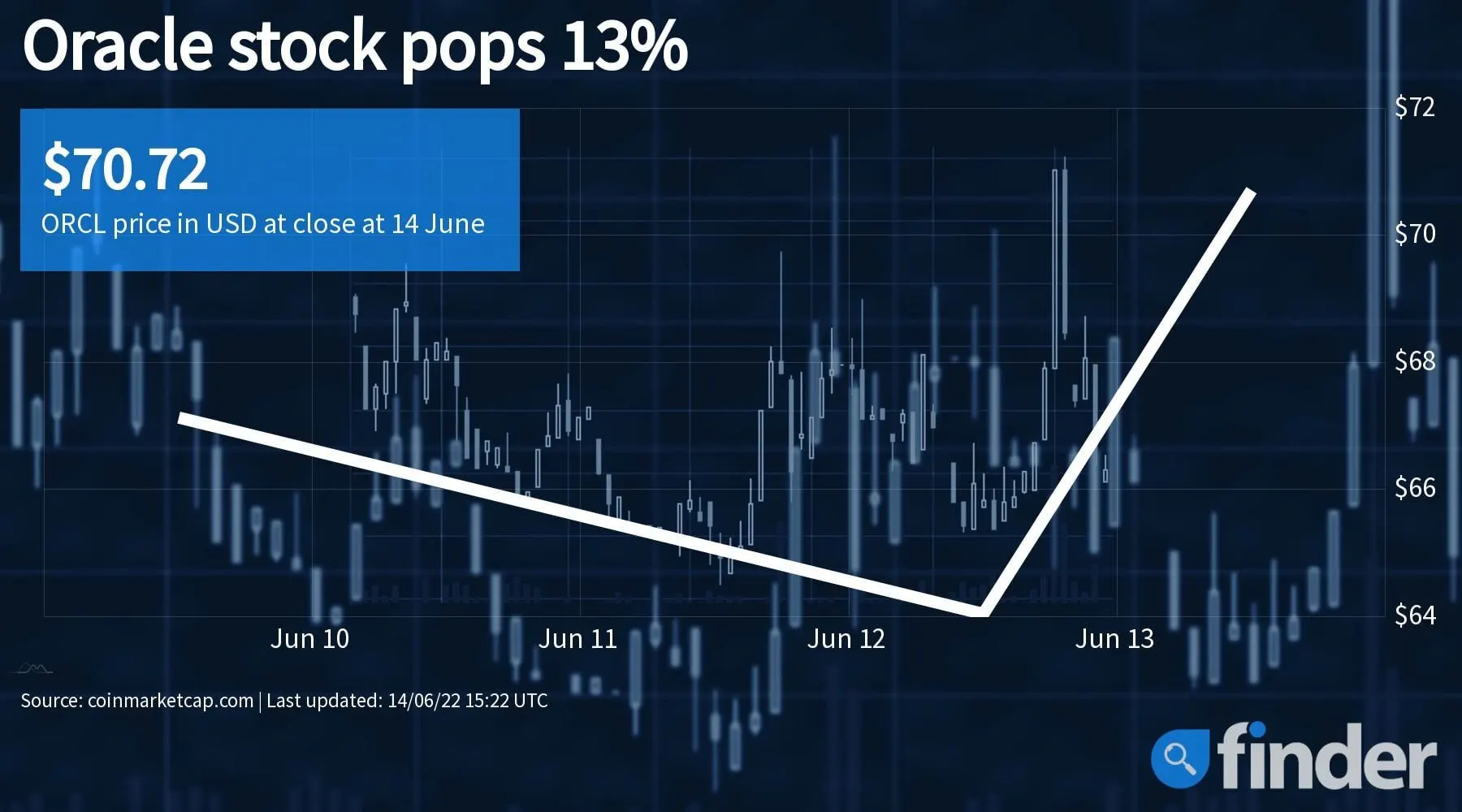

The stock jumped as much as 13% Tuesday, suggesting good results and positive guidance still matter in a market that can’t find its footing.

While positive news like this may not be enough to keep Oracle from falling along with the broader market over the short term, it may present a growth opportunity for when the market does eventually turn around.

The tech-heavy Nasdaq Composite was up slightly at the time of this writing Tuesday afternoon.

What happened?

Oracle reported better-than-expected earnings and revenue for its fiscal year 2022 fourth quarter, and the company sees this strength carrying into the quarters ahead despite current market conditions.

“Going forward and despite the macro environment, we continue to expect the revenue growth in our cloud business will accelerate substantially in fiscal year ’23,” Oracle CEO Safra Catz said during an earnings call Monday.

Total revenue for the quarter grew 5%, or 10% in constant currency, year over year to US$11.8 billion. This was driven by a large uptick, 22% in constant currency, of the company’s cloud revenue. Oracle said revenue from its cloud infrastructure, Oracle’s public cloud service launched in 2016, saw a major increase in demand and is becoming an increasingly important revenue stream for the company.

“We believe that this revenue growth spike indicates that our infrastructure business has now entered a hyper-growth phase,” Catz said in a statement. “Couple a high growth rate in our cloud infrastructure business with the newly acquired Cerner applications business — and Oracle finds itself in position to deliver stellar revenue growth over the next several quarters.”

Meanwhile, adjusted earnings were flat compared to the same quarter last year but came in above analysts’ estimates. Oracle reported adjusted earnings of US$1.54 per share, while Wall Street expected adjusted per share earnings of US$1.37.

Except for its hardware business, all of Oracle’s business segments grew from the prior year.

Oracle executives acknowledged during Monday’s earnings call the current and increasing macro uncertainty but remain optimistic about the business’s momentum. The company sees both revenue and earnings growing again in the current quarter, despite a 3% to 4% negative impact from persisting currency headwinds.

Oracle expects total revenue for its current quarter to grow from 17% to 19%, or from 20% to 22% in constant currency, and adjusted earnings of between US$1.04 and US$1.08, or US$1.09 and US$1.13 in constant currency.

For the full fiscal year 2023, Oracle said it expects cloud revenue, which grew 22% in fiscal 2022, will grow organically by more than 30% in constant currency. Including Cerner, the health information technology services company Oracle closed on last week, Oracle expects total cloud revenue to grow 47% to 50% in constant currency.

Thinking of buying Oracle stock?

Three of the four analysts that issued price target changes Tuesday lowered their expectations on Oracle stock, despite its stronger-than-expected earnings and outlook. This includes Stifel, BMO Capital and JP Morgan. Only Jefferies lifted their price target, which they raised from US$75 to US$80.

Even if Tuesday’s rally doesn’t last — which it likely won’t, seeing that most experts don’t think we’ve hit bottom yet — investors need to think about whether Oracle stock at this level signals a buy opportunity for when the market eventually does turn around.

The stock is down 34% from its previous high of US$106.34, and analysts on average see it returning to at least US$91.17 over the next 12 months. At about US$70 today, that would be a roughly 30% gain.

Looking for a low-cost online broker to invest in the stock market? Compare share trading platforms to start investing in stocks and ETFs.

Disclaimer: This information should not be interpreted as an endorsement of futures, stocks, ETFs, CFDs, options or any specific provider, service or offering. It should not be relied upon as investment advice or construed as providing recommendations of any kind. Futures, stocks, ETFs and options trading involves substantial risk of loss and therefore are not appropriate for all investors. Trading CFDs and forex on leverage comes with a higher risk of losing money rapidly. Past performance is not an indication of future results. Consider your own circumstances, and obtain your own advice, before making any trades.

At the time of publication, Matt Miczulski did not own shares of any equity mentioned in this story.

This news is republished from another source. You can check the original article here

Be the first to comment